ECO 1000 Lecture Notes

1 Four Principles

Objectives

- Apply cost-benefit principle to make decisions

- Compute opportunity costs

- Apply marginal principle to solve ‘how many’ problems

- Use interdependence principle to study how things interact with one another

1.1 Introduction

This lecture develops four tools that we will use throughout the course.

1.2 Cost-Benefit Principle

The cost-benefit principle is very simple: if the benefits of something outweigh the costs, do it. If not, don’t.

1.3 Opportunity Cost Principle

The opportunity cost principle states that the true cost of something is what you give up to get it. This is an important ‘clarification’ tool. When deciding how happy we are with our choice, we don’t need to consider all the things we gave up, just the next best alternative.

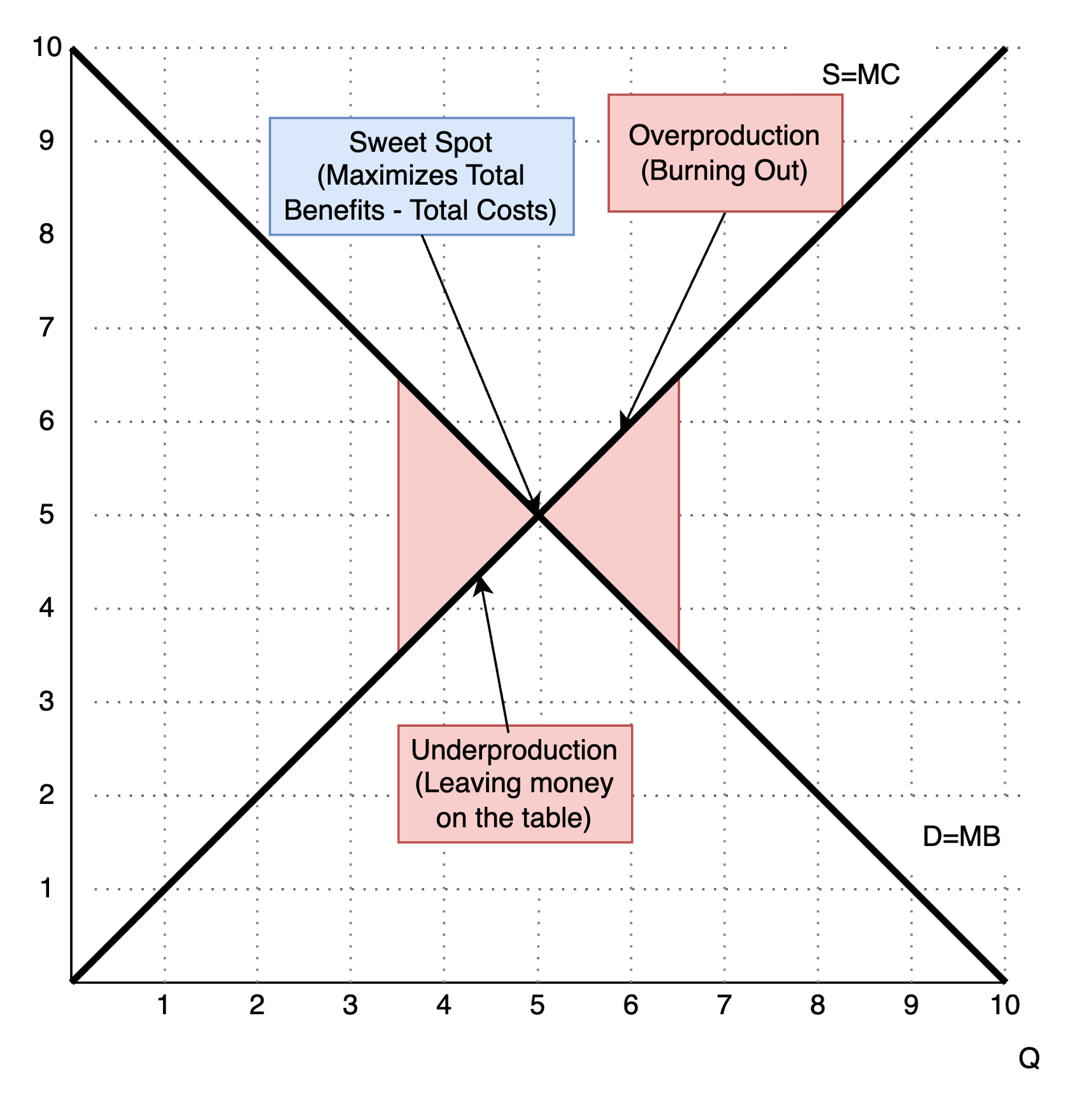

1.4 Marginal Principle

The marginal principle helps us solve a very important class of problems: how many of something should we do? When solving these problems, we need to consider the extra (marginal) costs and benefits of doing a little more or a little less of something.

We approach this by computing the marginal benefit and cost of each additional unit. In the example, our total benefit moving from 0 to 1 loaf of bread is 15, so the marginal benefit of the first loaf is 15. Our total cost moving from 0 to 1 loaf of bread is 2, so the marginal cost of the first loaf is 2. Moving from 1 loaf to 2 loaves, our total benefit increases from 15 to 25, so the marginal benefit of the second loaf is 10. Moving from 1 loaf to 2 loaves, our total cost increases from 2 to 10, so the marginal cost of the second loaf is 8.

In this case, we maximize our total surplus by producing 2 loaves of bread. If we produce 3 loaves, our marginal cost (10) exceeds our marginal benefit (7). This produces a decrease in our total surplus of 3, so we are worse off.

| # Loaves of Bread | Total Benefit | Total Cost | Marginal Benefit | Marginal Cost | Total Surplus |

|---|---|---|---|---|---|

| 0 | 0 | 0 | 0 | ||

| 1 | 15 | 2 | 15 | 2 | 13 |

| 2 | 25 | 10 | 10 | 8 | 15 |

| 3 | 32 | 20 | 7 | 10 | 12 |

From the marginal principle, we develop the rational rule, which prescribes how to make optimal decisions:

1.5 Interdependence Principle

The interdependence principle helps us classify outside factors that influence our decisions. We will often focus on a a few key factors, such as the price of a good, and hold everything else constant. The interdependence principle categorizes some of these outside factors.

1.6 Conclusion

- This lecture develops four tools to use within economics

- Cost-Benefit Principle: what choice should we make?

- Opportunity Cost: what are we giving up?

- Marginal Principle: how much should we do something?

- Interdependence Principle: what else does our decision depend on?