4 Exchange Rates

Objectives

- Be able to define the exchange rate

- Understand the impact of exchange rate appreciation / depreciation on trade flows

- Compute the change (appreciation or depreciation) of an exchange rate

- Understand arbitrage conditions

- Two currencies, three currencies, covered and uncovered interest rate parity

4.1 Introduction

| Exchange Rate | Appreciates | Depreciates |

|---|---|---|

| EUSD/EUR | Decreases ↓ | Increases ↑ |

| Verbal Intuition | ‘It takes less Dollars to buy a Euro → Dollar is more powerful’ | ‘It takes more Dollars to buy a Euro → Dollar is less powerful’ |

| USD Exchange Rate | Appreciates | Depreciates |

|---|---|---|

| E$/€ | Decreases ↓ | Increases ↑ |

| U.S. Exports | Decreases ↓ One Euro buys less stuff in U.S., so U.S. exports less |

Increases ↑ One Euro buys more stuff in U.S., so U.S. exports more |

| U.S. Imports | Increases ↑ Euros are cheaper, so U.S. imports more from Europe |

Decreases ↓ Euros are more expensive, so U.S. imports less from Europe |

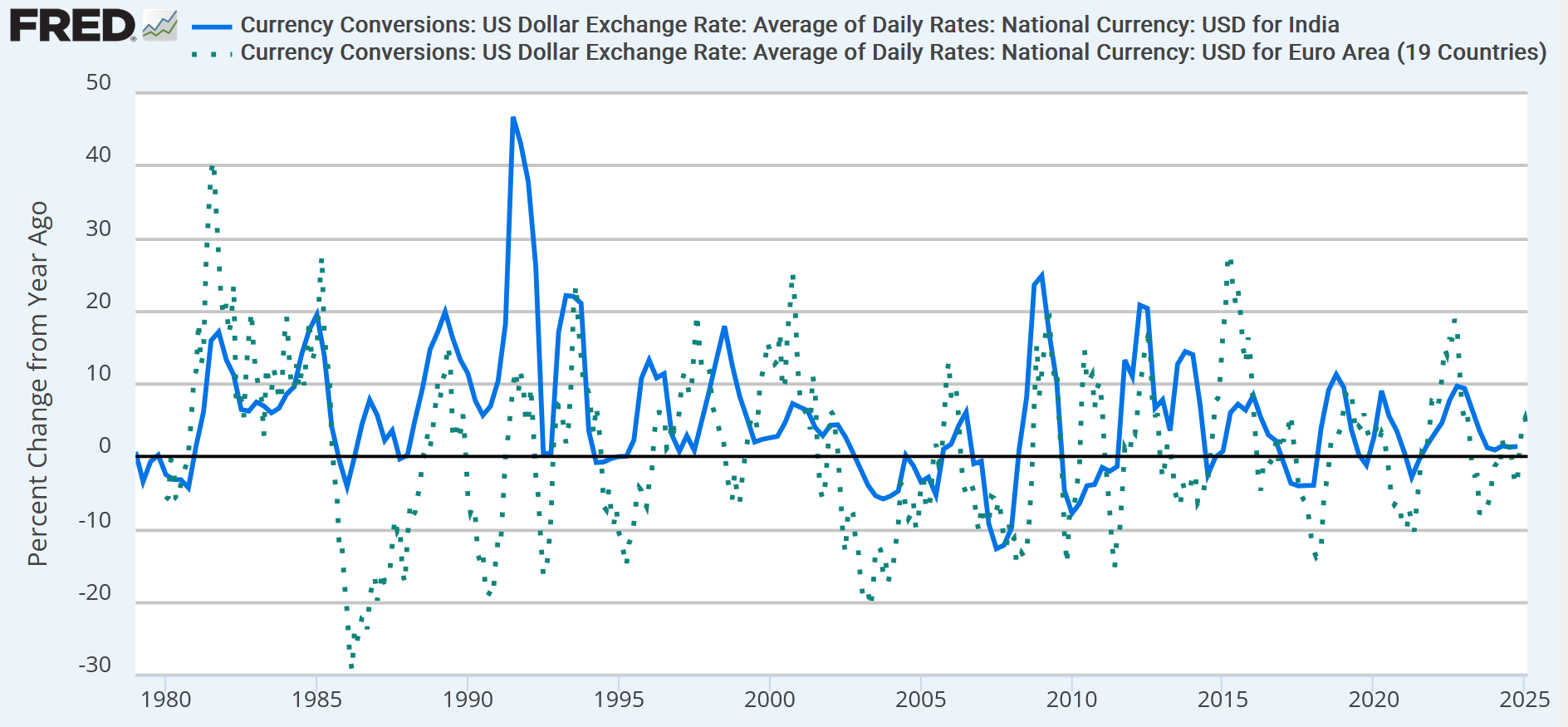

4.2 Growth Rate

We typically evaluate the ‘change’ of the exchange rate by looking at its growth rate over time. \[ \text{GR}_{E} = \frac{ E_{\text{new}} - E_{\text{old}} }{ E_{\text{old}} } \times 100 \]

The benefit of using the growth rate is that it makes the change comparable i) over time and ii) across countries.

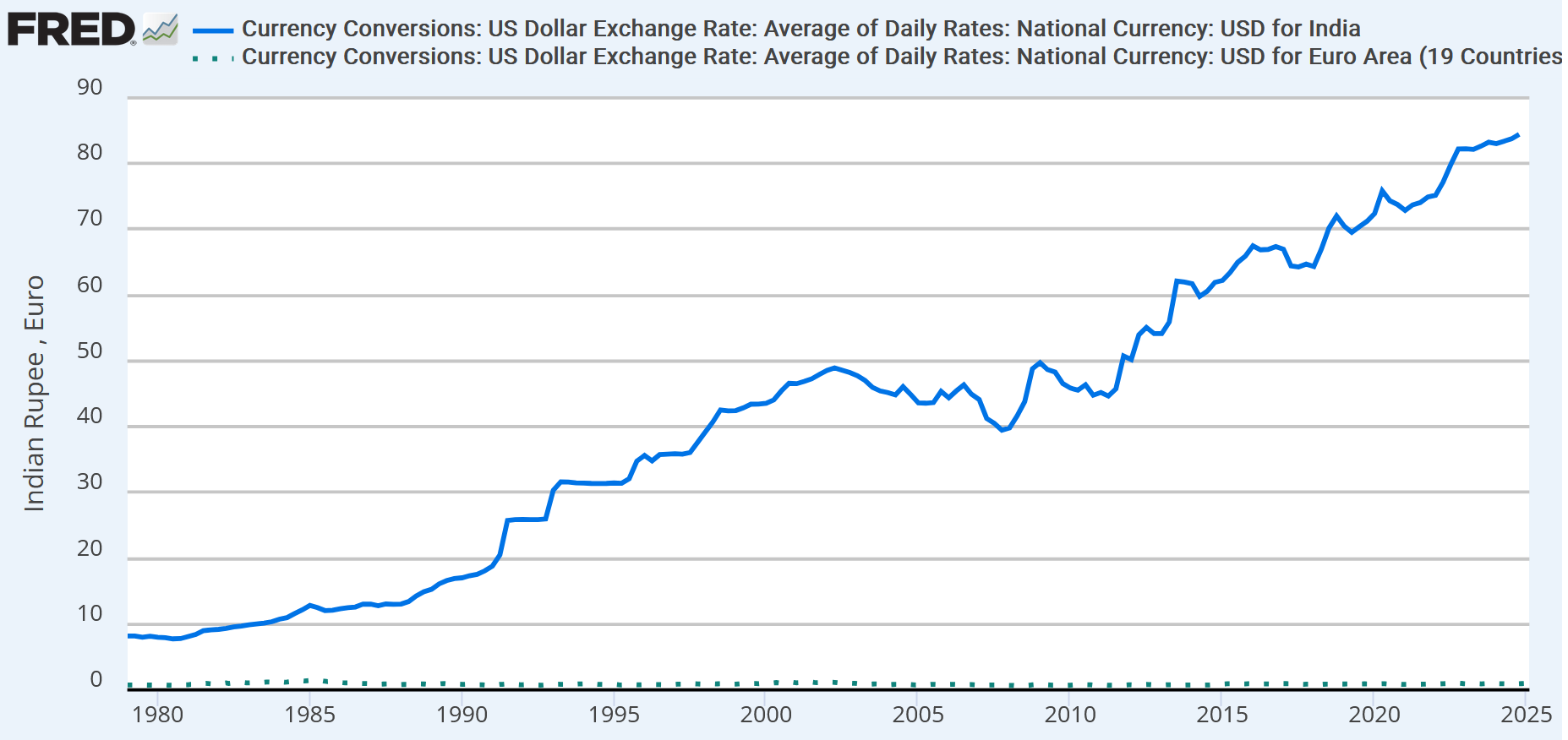

We can see this by comparing the \(E_{USD/EUR}\) (Euro) and \(E_{USD/INR}\) Indian Rupee exchange rates. In levels, the \(E_{USD/INR}\) exchange rate is inflated compared to the \(E_{USD/EUR}\) exchange rate, so the two series are not comparable. When we apply the growth rate transformation, we can compare the two exchange rates directly.

4.3 Arbitrage: Currencies

This section will discuss arbitrage in the context of exchange rates. Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Simply put, we buy something in a market and sell it in another for a higher price. The only change is that the ‘good’ we buy is a currency, and the markets are the foreign exchange markets. There are many arbitrage opportunities outside of international finance. A classic example is resellers buying clothing in a thrift store and selling them on eBay.

| Term | Definition |

|---|---|

| Spot Contract | An exchange where the price is settled today and the exchange occurs immediately |

| Forward Contract | An exchange where the price is settled today and the exchange occurs in the future |

4.3.1 Arbitrage: Two Currencies

We first consider the case of arbitrage with two currencies. Suppose we can buy a Euro using Dollars in New York and Paris. In New York, the exchange rate is \(E_{USD/EUR}^{\text{New York}} = \$3\). In Paris, the exchange rate is \(E_{USD/EUR}^{\text{Paris}}= \$1\).

In this case, the ‘good’ is a Euro, and we have different ‘prices’ of the Euro in two different markets: New York and Paris. Our strategy is to buy the Euro where it is cheap, in Paris. We then sell where it is expensive, in New York. Using this strategy, our initial one Dollar becomes three Dollars.

4.3.2 Arbitrage: Three Currencies

We now consider the case of three currencies. Suppose the Euro/US Dollar exchange rate is \(E_{EUR/USD} = 0.8 EUR / USD\) and the British Pound / Euro exchange rate is \(E_{GBP/EUR} = 0.7 GBP / EUR\).

Imagine the ‘direct’ Pound to Dollar market is closed. In this case, we take the indirect path of first purchasing Euros with Pounds, and then Dollars with Euros. How much does this cost us? To buy a Dollar, we need \(0.8 EUR\). To buy that many Euros, we need \(0.8 EUR \times 0.7 GBP / EUR = 0.56 GBP\). To buy a single Dollar, we need \(0.56\) Pounds. This is the ‘indirect’ way to purchase a Dollar that involves visiting one additional market.

Now suppose the ‘direct’ Pound to Dollar market opens, and the price is \(E_{GBP/USD} = 0.50 GBP / USD\). We now have two ways to buy a Dollar, with different prices. Under the direct method, a Dollar costs 0.50 GBP. Under the indirect method, a Dollar costs 0.56 GBP. We therefore have an arbitrage opportunity.

The intuition is the same as with the two currency example: buy the Dollar in the cheap market and sell the Dollar in the expensive market. In this case, we would buy the Dollar using the direct method for 0.50 GBP. We would then sell using the indirect method to gain 0.56 GBP. Overall, we profit 0.06 GBP.

4.4 Arbitrage: Interest Rates

This section examines arbitrage for interest rates. Interest rates are prices, just like exchange rates. In this case, the interest rate is the price of borrowing money from a lender.

For instance, if you take a one-year loan of $10,000 with an interest rate of 5%, your one-year ‘price’ of borrowing the money (you have to pay it back!) is $500. This section will examine arbitrage opportunities that arise in interest rate differences across countries.

We introduce U.S. and European interest rates \(i_{USD}\) and \(i_{EUR}\). Assume the current exchange rate and forward rate are \(E_{USD/EUR}\) and \(F_{USD/EUR}\).

4.5 Covered Interest Parity

Suppose we have one Dollar and must decide where to save it. If we save in the U.S., we simply receive \(i_{USD}\), so in one year we have \(1 + i_{USD}\).

Now suppose we see a higher interest rate in Europe, and consider saving in Euros. This presents two problems: we can only save in Euros, and we can only buy things within the U.S. using Dollars. We will therefore have to i) convert to Euros to save and ii) convert back to Dollars afterwards.

We start by converting our Dollar to Euros, this provides \(\frac{1}{E_{USD/EUR}}\) Euros. Next, we earn interest on the Euros, which provides \((1 + i_{EUR}) \frac{1}{E_{USD/EUR}}\). Finally, we convert back to Dollars using the forward. This provides \((1 + i_{EUR}) \frac{F_{USD/EUR}}{E_{USD/EUR}}\).

Covered Interest Parity compares the return on saving our Dollar in the U.S. with the return on saving our Dollar in Europe.

4.6 Uncovered Interest Parity

Uncovered Interest Parity follows the same logic as Covered Interest Parity, but assumes a forward \(F\) is not available. When we need to convert our Euros back to Dollars, we use our ‘expectation’ of the future exchange rate \(E_{USD/EUR}^e\). Note that covered interest parity provided a certain return, because the forward is predetermined, but uncovered interest parity does not provide a certain return.

4.7 Conclusion

This section has introduced the concept of exchange rates. We apply the growth rate concept to study how exchange rates change over time. We then introduce the concept of arbitrage, and apply it to exchange rates and interest rates to provide more structure. Arbitrage for the exchange rate is provided by two and three currency arbitrage. Arbitrage for interest rates is provided by covered and uncovered interest parity.