5 Welfare

Objectives

- Compute consumer surplus and total consumer surplus

- Compute producer surplus and total producer surplus

- Compute economic and total economic surplus

- Identify optimal levels of producing, underproducing, and overproducing

5.1 Introduction

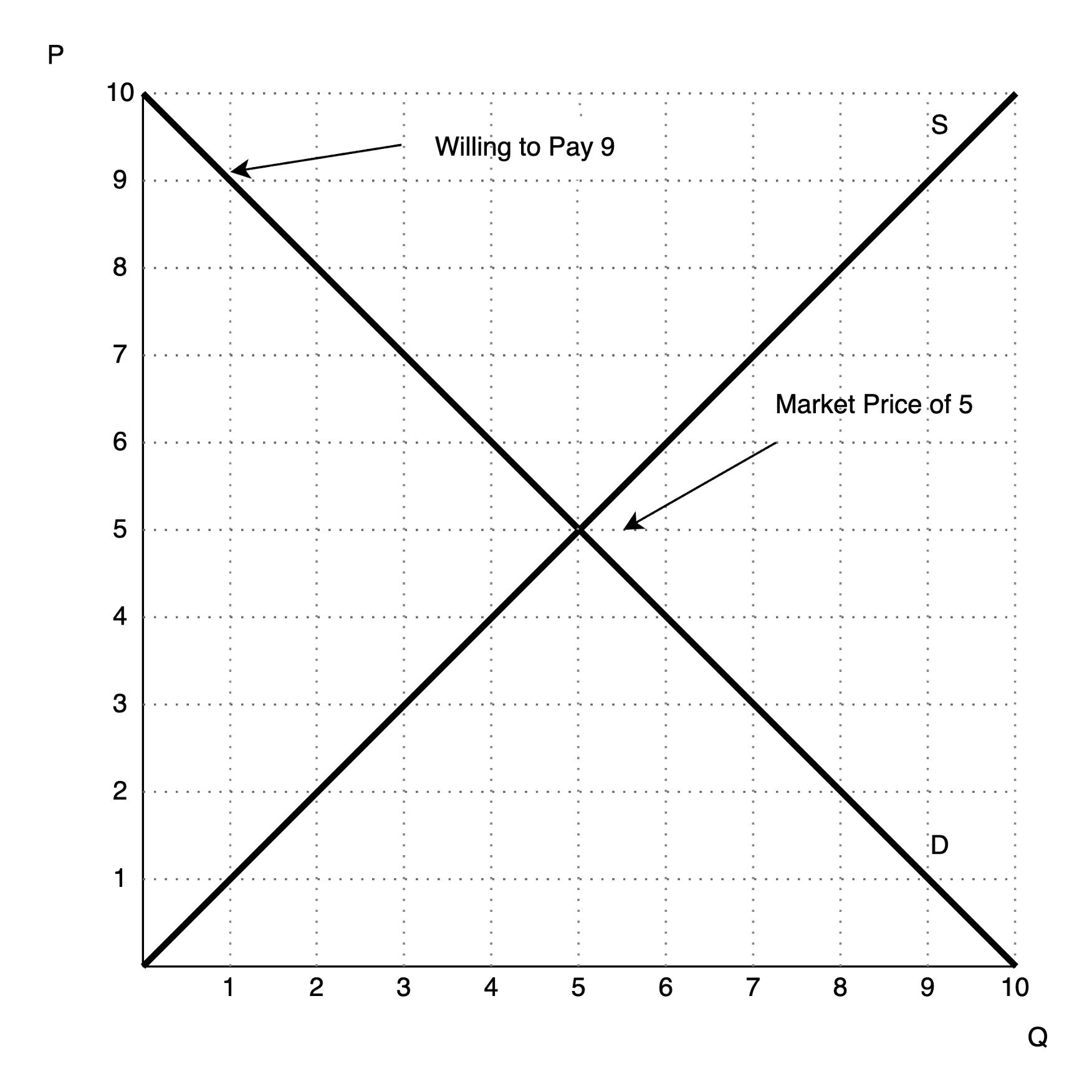

This section studies welfare, how ‘happy’ we are from engaging with the market. Let’s considert the following simple market equiliibrium:

In this case we have an equilibrium price of 5 and quantity of 5. If we look closely, the quantity demanded when the price was equal to \(\$9\) is \(1\). More specifically, someone was willing to pay \(\$9\) for one unit of the good. Are they happy? Yes: they were willing to pay \(\$9\) but only had to pay \(\$5\), so they are \(\$4\) better off.

If we visit the producers, a producer was willing to provide a unit when the price was \(\$1\). are they happy? Yes: they were willing to produce it for \(\$1\) but received \(\$5\).

We therefore have winners on both the consumer side and the producer side of the market. Our goal is to develop a measure of how ‘happy’ they are, which we simple call welfare or their surplus.

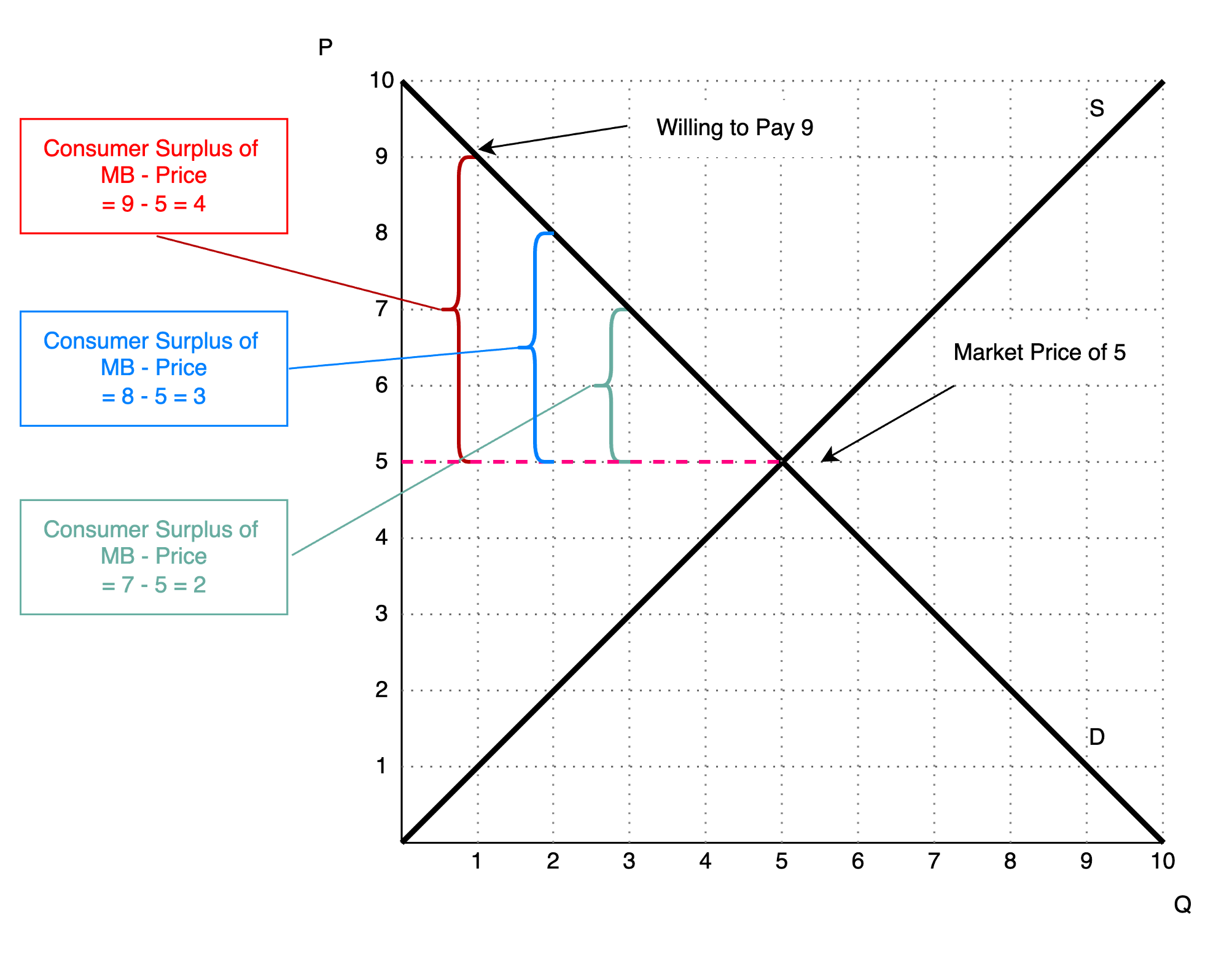

5.2 Consumer Surplus

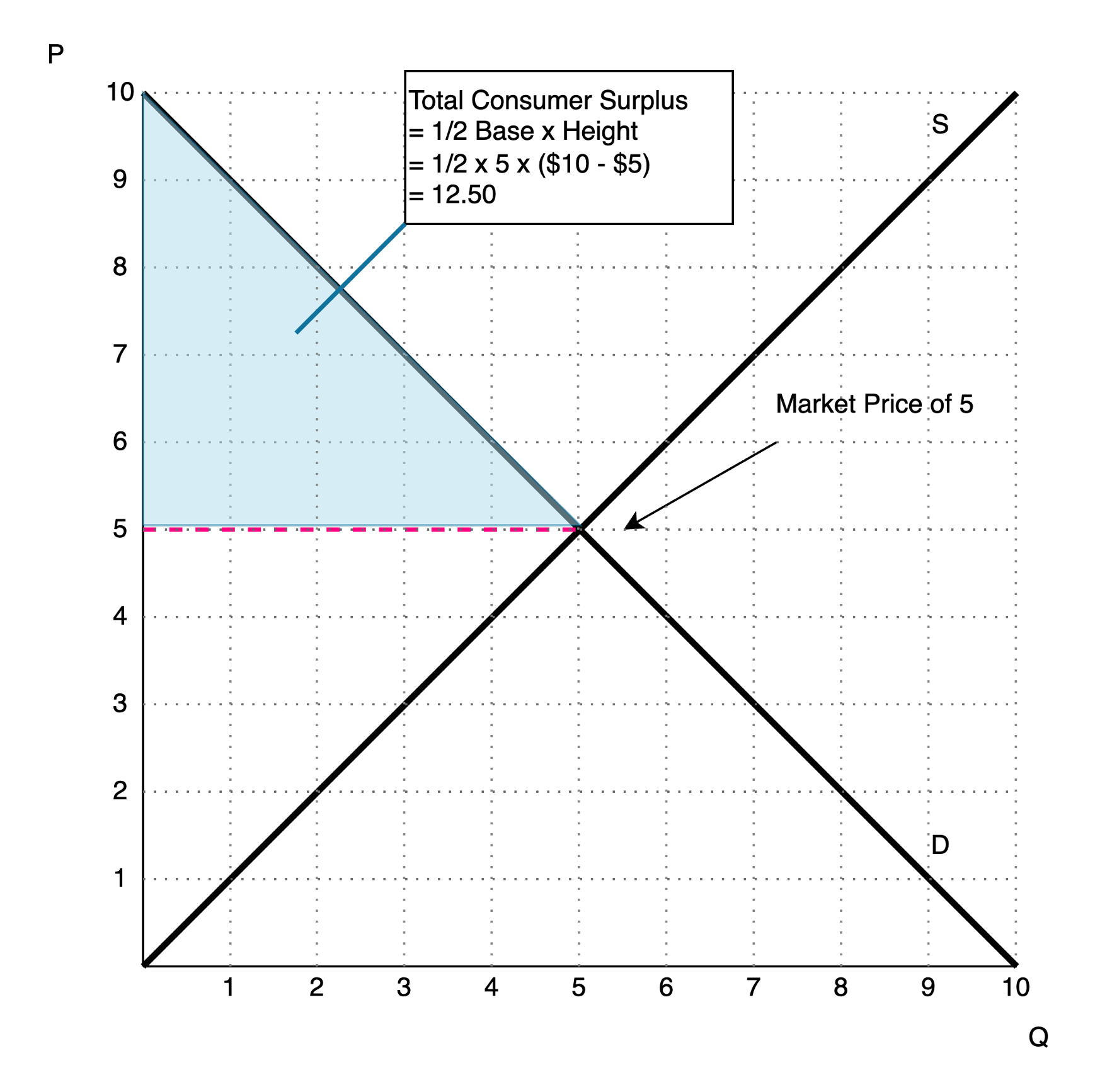

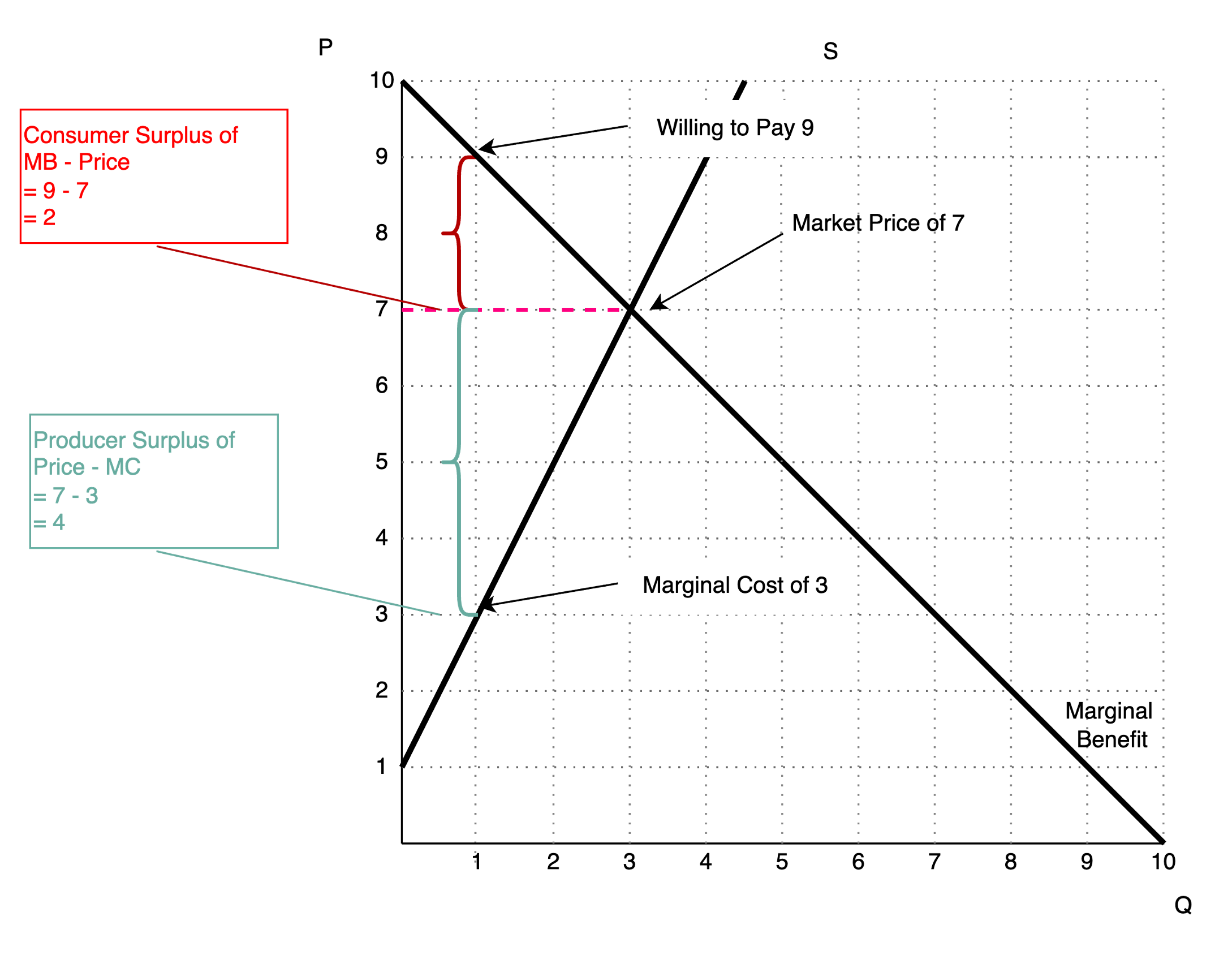

We will measure how happy consumers are by computing the consumer surplus, where we interpret surplus as what you have ‘leftover’ from the market. The left hand side shows how to compute the consumer surplus for single units. We compute the total consumer surplus by summing the consumer surplus for all units purchased, as shown on the right hand side. We will ‘squint’ and simply compute the area under the demand curve and above the price, which is a triangle.

Individual and Total Consumer Surplus

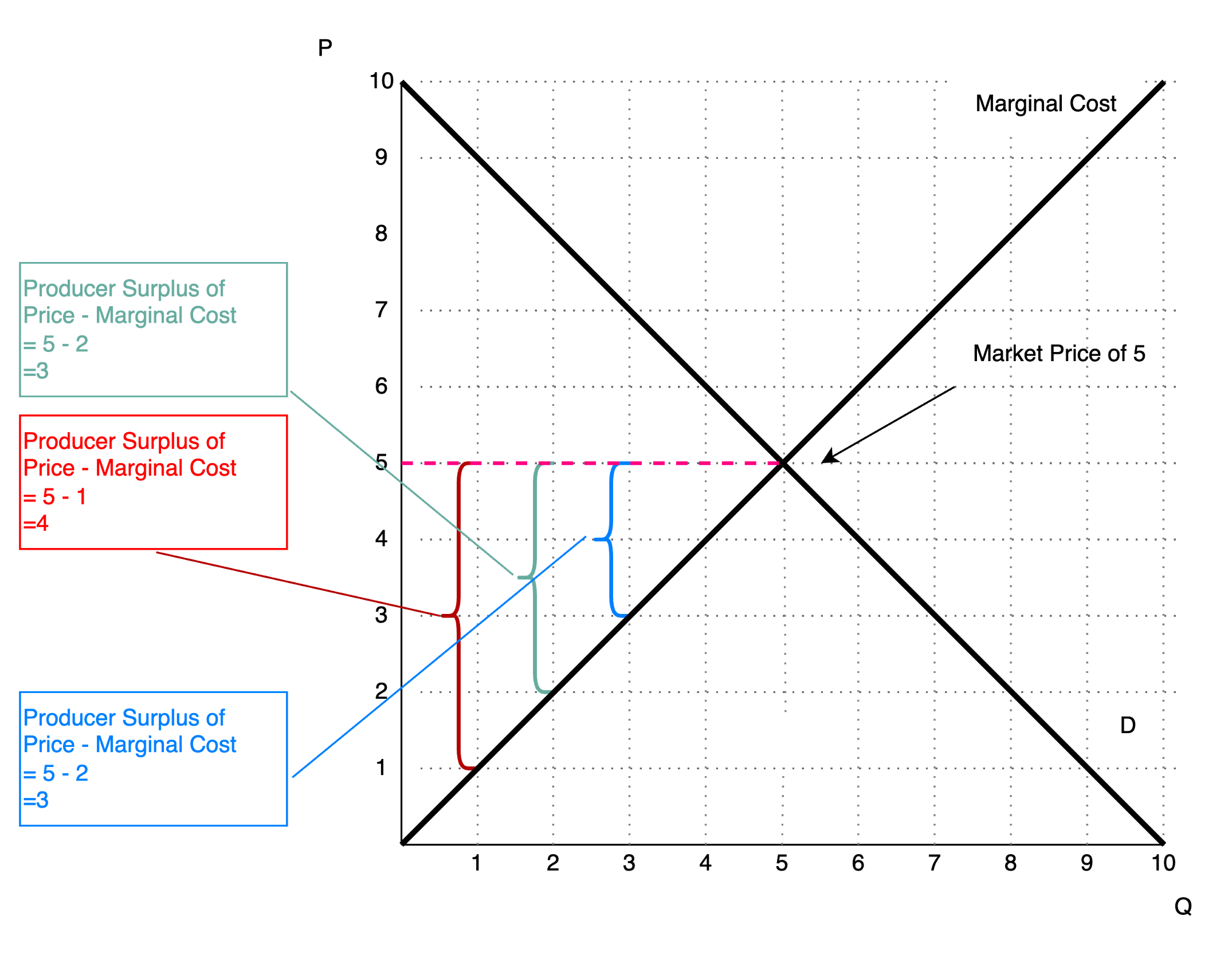

5.3 Producer Surplus

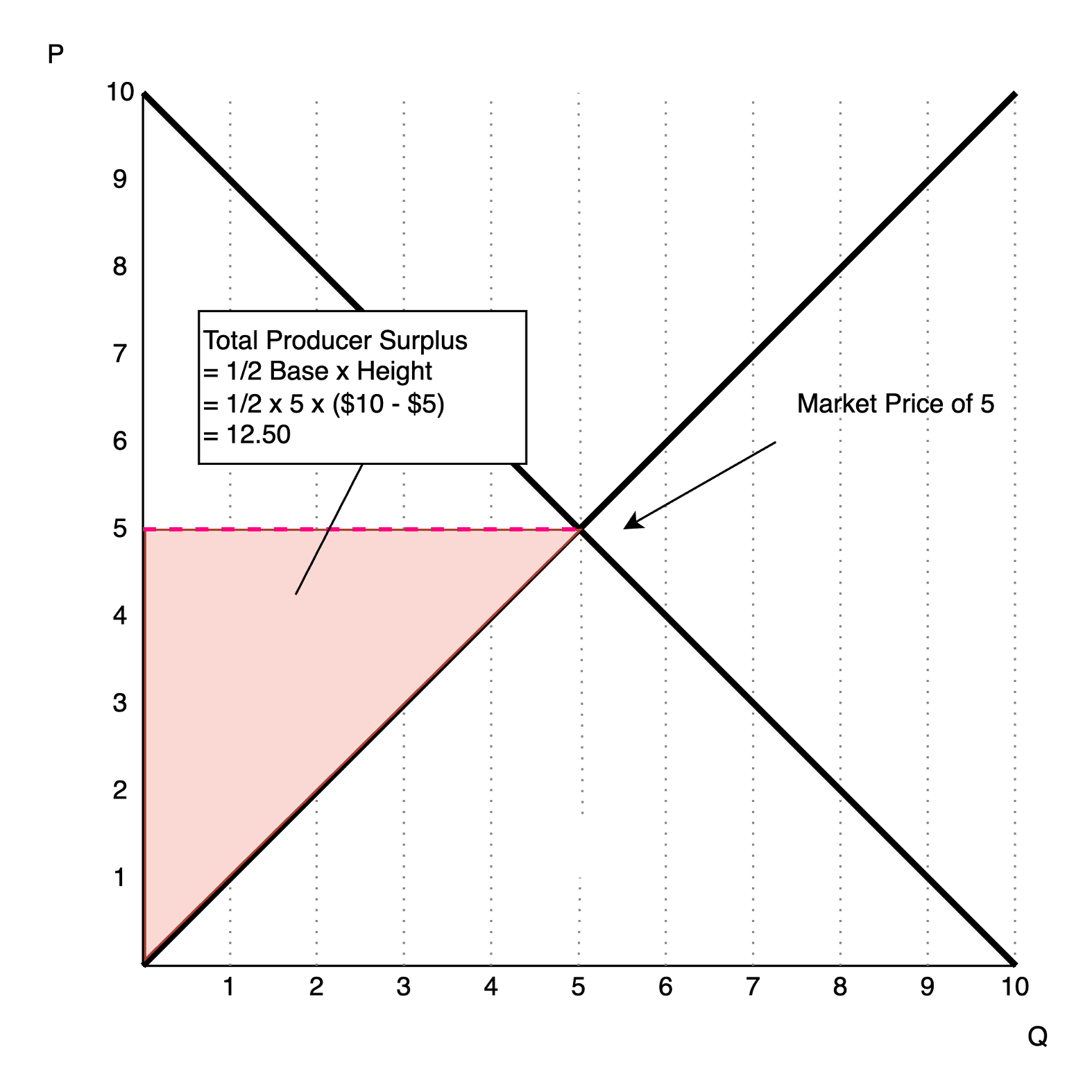

Are producers happy? The first producer sold the good for \(\$5\) but their marginal cost was only \(\$1\), so they are \(\$4\) better off. The second producer sold the good for \(\$5\) but their marginal cost was only \(\$2\), so they are \(\$3\) better off. We compute the producer surplus by calculating the difference between the price and the marginal cost for each unit sold. We compute the total producer surplus by summing the producer surplus for all units sold, as shown on the right hand side. As with consumer surplus, we will ‘squint’ and compute the area above the supply curve and below the price, which is a triangle.

Individual and Total Producer Surplus

5.4 Economic Surplus

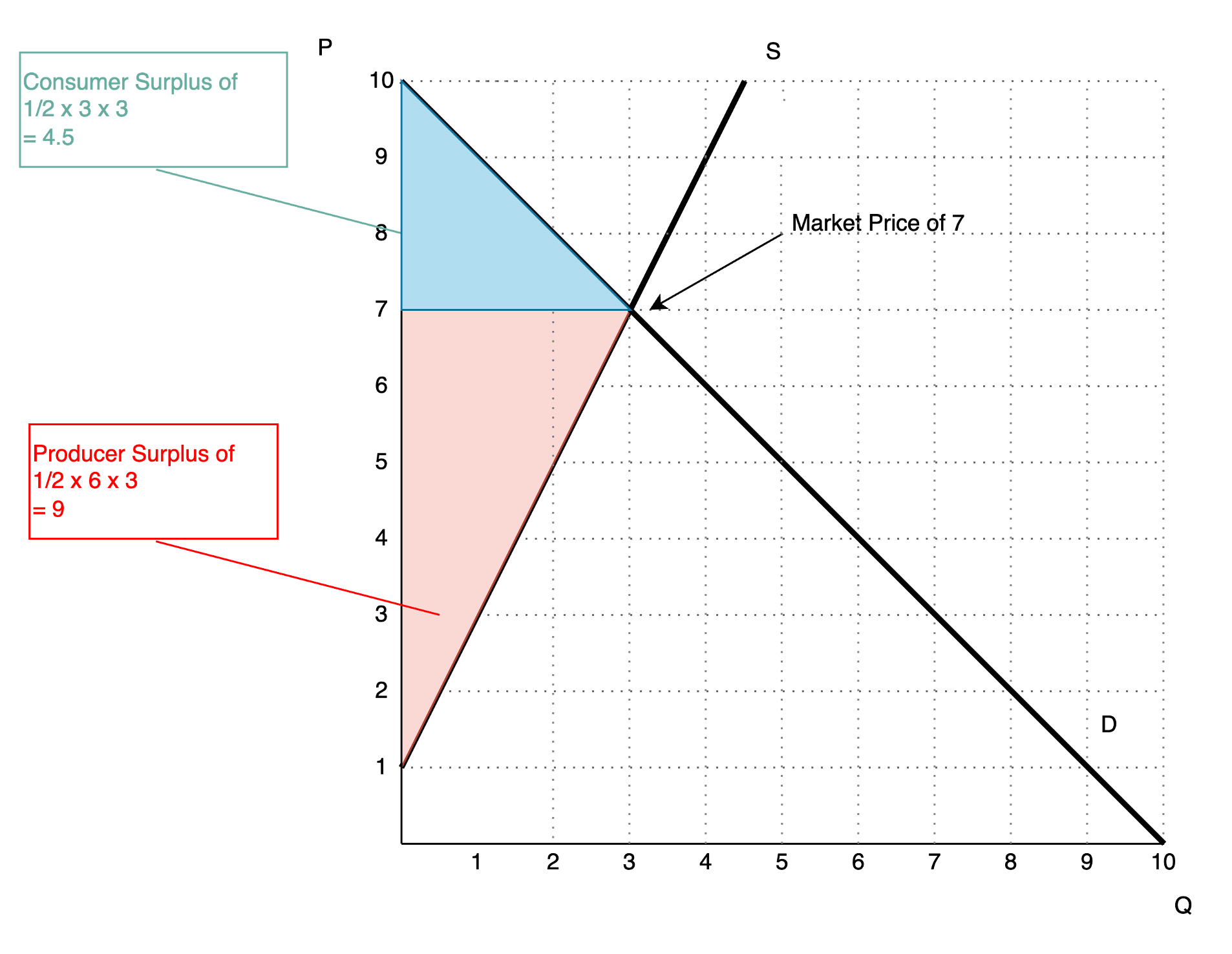

We now want to measure the welfare of all market participants (consumer + producer). The economic surplus is the sum of the consumer surplus and producer surplus for each unit. Notice we can compute it as: \[ \text{Economic Surplus} = (MB - P) - (P - MC) = MB - MC. \] The price cancels out and we are left with marginal benefit minus marginal cost.

The total economic surplus is simply the sum of the total consumer surplus and total producer surplus.

Individual and Total Economic Surplus

5.5 Efficiency

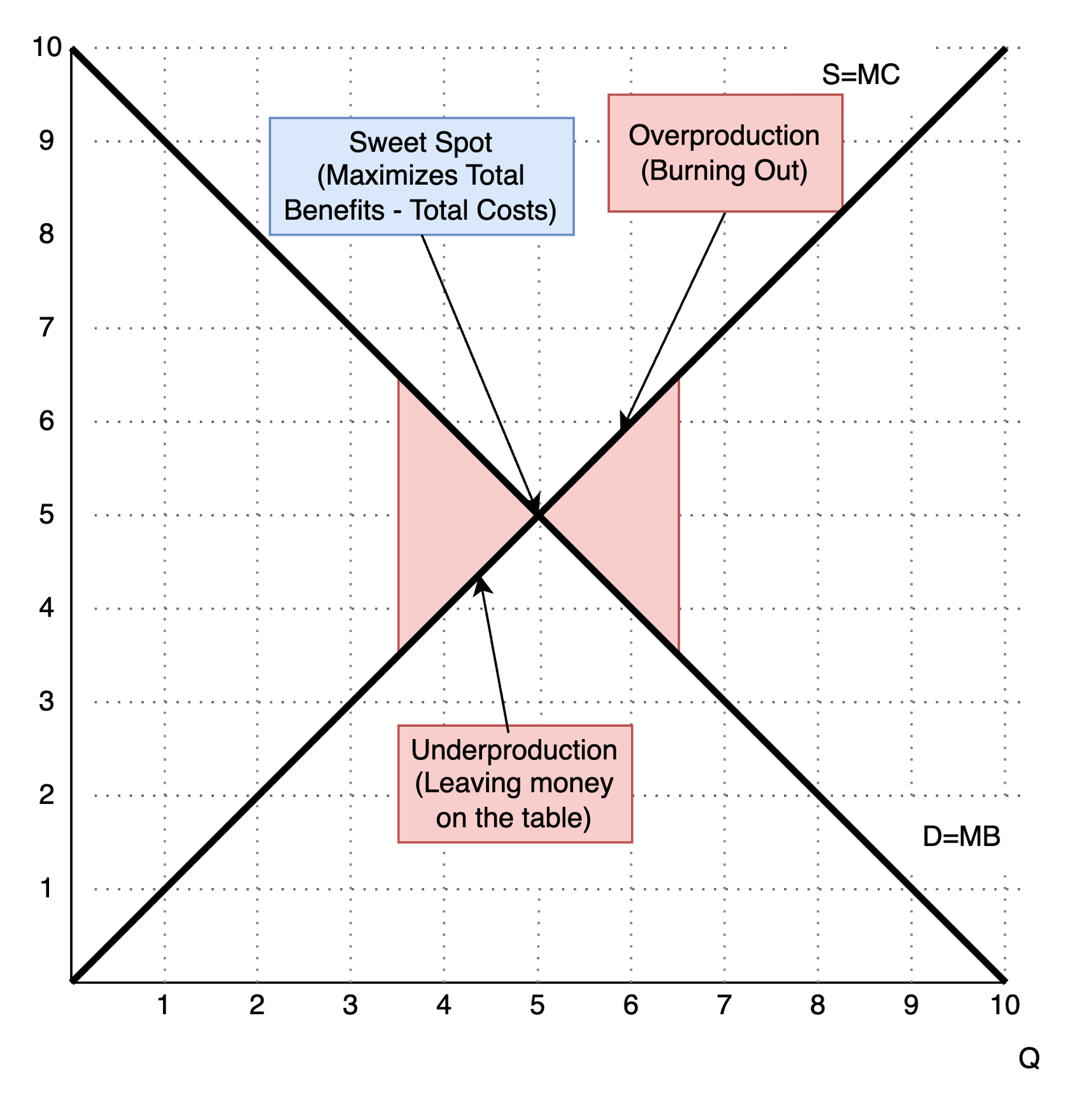

We now consider the overal lefficiency of the market. We know the demand curve is equal to the marginal benefit curve and the supply curve is equal to the marginal cost curve. How much should we produce? The rational rule for society is to produce the quantity where marginal benefit equals marginal cost. But within our market, this is precisely where supply is equal to demand, the equilibrium. This is one of the most important results in economics: the market equilibrium maximizes welfare or total economic surplus.

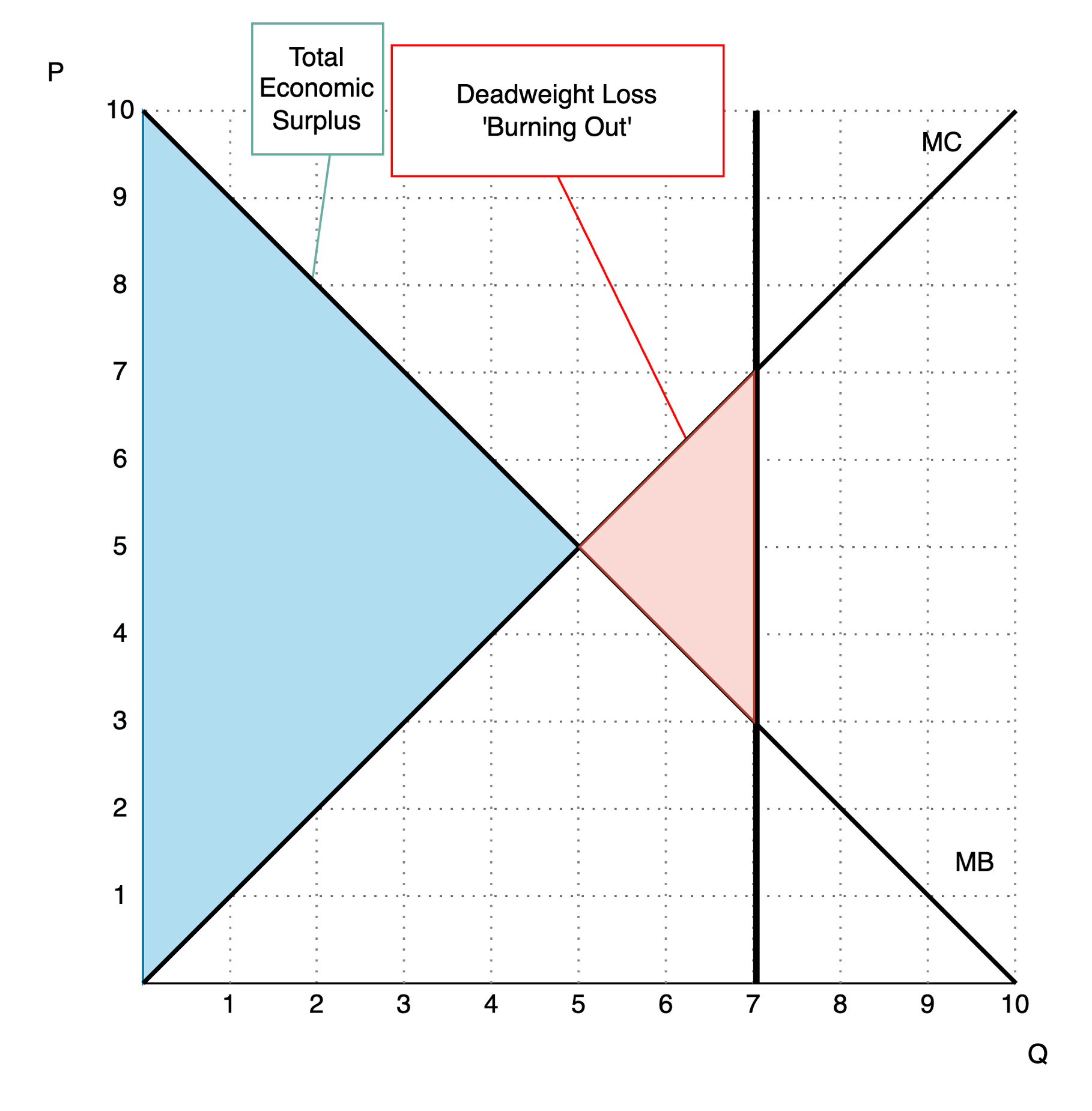

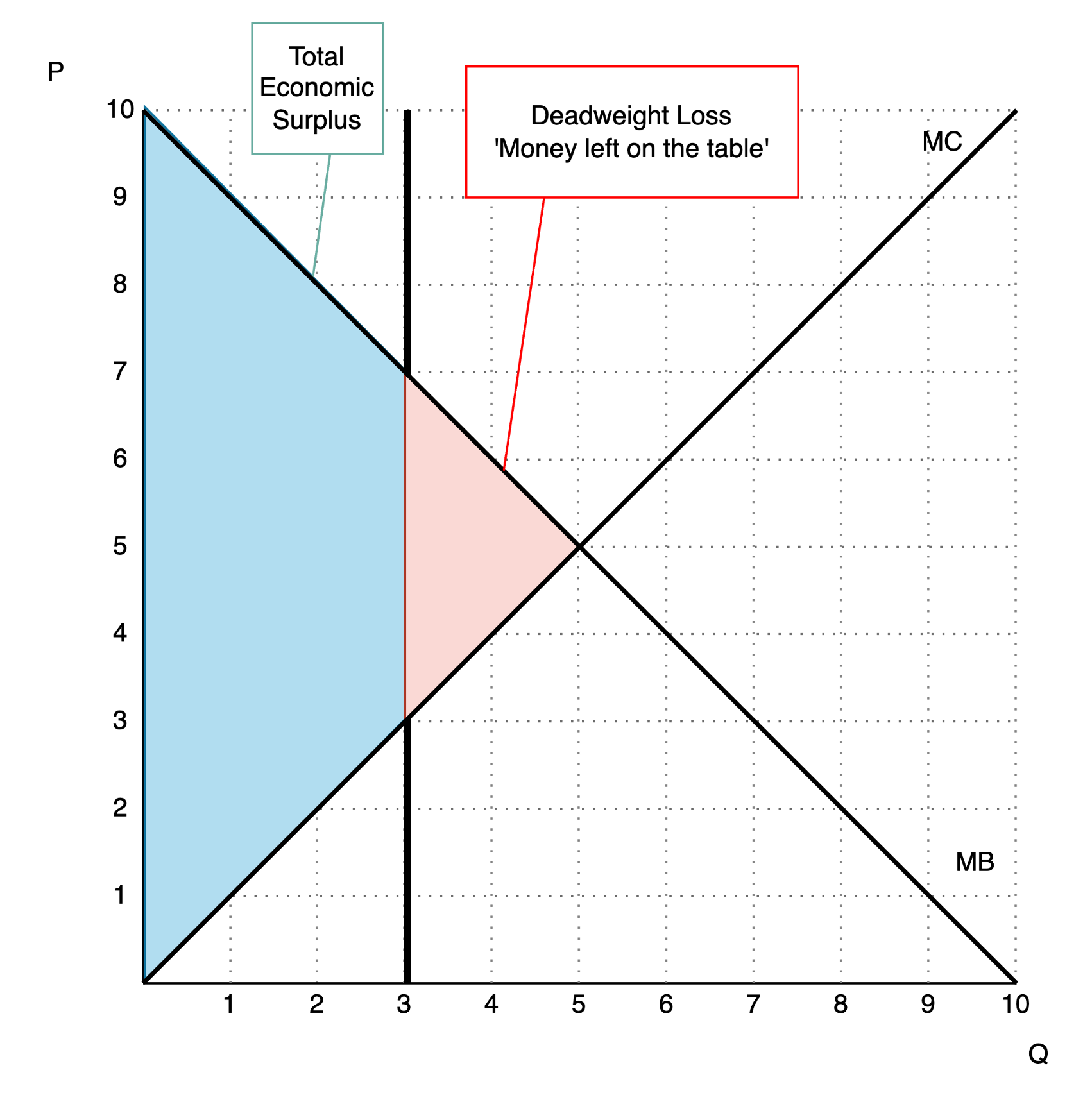

We now consider two unoptimal cases: overproducing and underproducing. In the first case, our marginal cost exceeds our marginal benefit, so we are producing too much. In the second case, our marginal benefit exceeds our marginal cost (we should take one step forward), so we are producing too little.

Unoptimal: Over and underproduction

5.6 Conclusion

- This lecture develops our measures of welfare

- How ‘happy’ we are from engaging with the market

- On the consumer side, we compute the consumer surplus

- On the producer side, we compute the producer surplus

- We compute the welfare of all market participants (consumer + producer) by combining for the economic surplus

- We show that the market equilibrium maximizes the total economic surplus or welfare